Accounting System

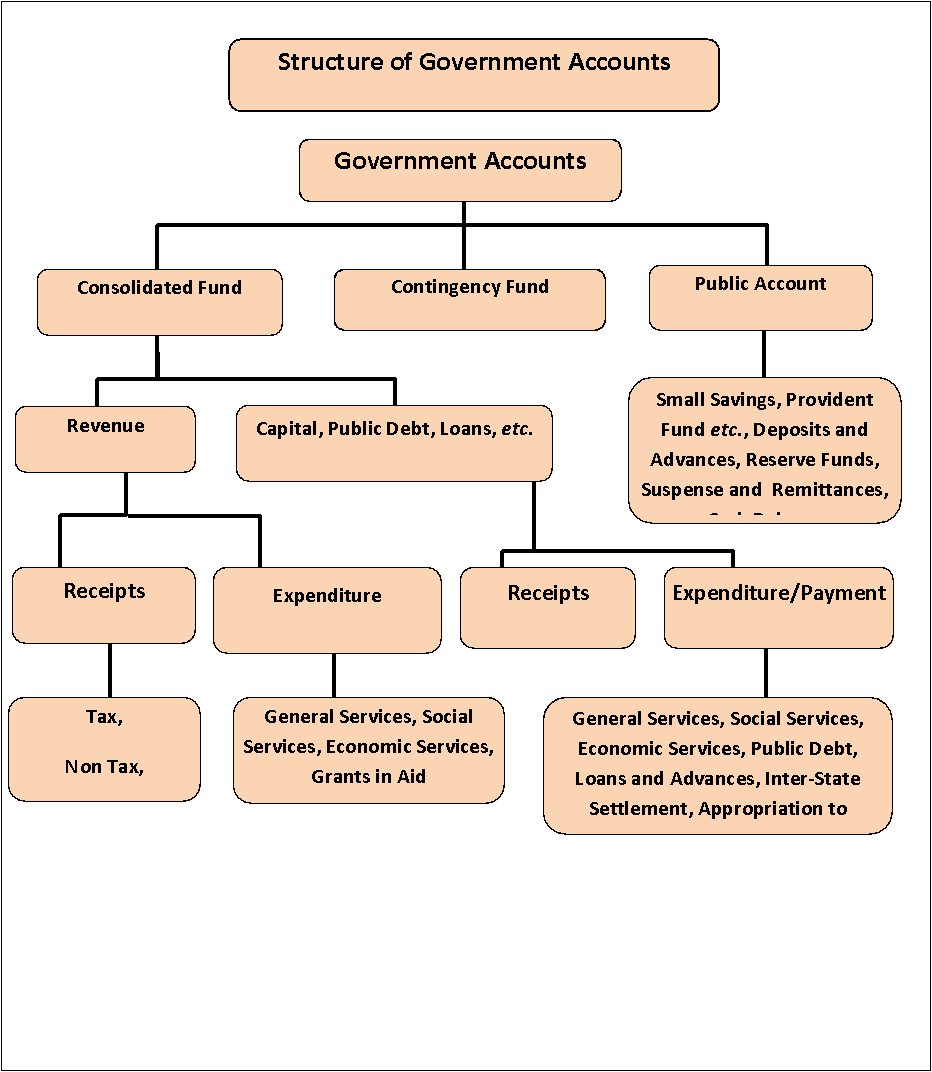

Division of Accounts : The accounts of Government are kept in the following three parts:

- Part I Consolidated Fund

- Part II Contingency Fund

- Part III Public Account

There are two main divisions under the Consolidated Fund:

The Revenue division (Revenue Account) deals with the proceeds of taxation and other receipts classed as revenue and the expenditure met there from, the net result of which represents the revenue surplus or deficit for the year.

In the Capital division, the section ‘Receipt Heads (Capital Account)’ deals with receipts of capital nature that cannot be applied as a set off to capital expenditure. The section ‘Expenditure Heads (Capital Account)’ deals with expenditure met usually from borrowed funds with the object of increasing concrete assets of a material and permanent character. It also includes receipts of a capital nature that are applied as a set off to capital expenditure. The section ‘Public Debt, Loans and Advances, etc.’ comprises loans raised and their repayments by Government such as ‘Internal Debt’ and ‘Loans and Advances’ made (and their recoveries) by Government.

In the Contingency Fund, the transactions connected with Contingency Fund established under Article

In the Public Account, the transactions relating to ‘Debt’ (other than those included in Part I), ‘Deposits’, ‘Advances’, ‘Remittances’ and ‘ Suspense’ are recorded. The transactions under 'Debt', 'Deposits' and 'Advances', in this part are those in respect of which Government incurs a liability to repay the moneys received or has a claim to recover the amounts paid, together with the repayments of the former ('Debt', and 'Deposits') and the recoveries of the latter ('Advances'). The transactions relating to 'Remittances' and 'Suspense' in this part embrace merely adjusting heads under which appear such transactions as remittances of cash between treasuries and currency chests, transfers between different accounting circles, etc. The initial debts or credits to these heads will be cleared eventually by corresponding receipts or payments either within the same circle of account or in another account circle.